Holiday Rentals in the Valencian Community: Tax Strategies and Pitfalls for Non-Residents 2026

The Valencian Community – from the picturesque Costa Blanca to the vibrant metropolis of Valencia – remains a magnet for real estate investors worldwide. But the dream of returns through holiday rentals is closely tied to Spanish bureaucracy. For non-residents, understanding the tax rules is essential to avoid falling into the trap of double taxation or paying unnecessary levies.

1. The Tax System: IRNR and the Owner's Origin

In Spain, property owners whose tax residence is abroad are subject to Non-Resident Income Tax (IRNR). There is a strict division here:

EU Citizens (e.g., Germany, Austria)

Tax rate: 19% on net profit.Privilege: They can deduct all costs directly related to the rental for tax purposes. This includes cleaning, proportional utility costs, mortgage interest, and building depreciation (3% per year).

Non-Residents from Third Countries (e.g., Switzerland, Great Britain)

Tax rate: 24% on gross income.Challenge: Since Brexit (for the UK) or due to third-country status (Switzerland), Spanish law does not allow any cost deductions. Every euro earned is taxed at 24%, regardless of how high your expenses for maintenance or administration were.

2. The Specter of Double Taxation: How You Are Protected

Many investors fear that their rental income will be fully taxed in both Spain and their home country. This is where the so-called Double Taxation Agreements (DTA) come into play.

How does the protection work?

According to the agreements between Spain and countries like Germany, Austria, or Switzerland, Spain, as the state where the property is located, has the primary right of taxation.

Tax payment in Spain: You first declare and pay tax on your rental income in Spain (Modelo 210).Declaration in your home country: You must also mandatorily declare this income in your domestic tax return.

Credit method: To avoid double taxation, the tax paid in Spain is usually credited against the tax liability in the home country, or the income is exempted (subject to progression). The exact handling depends on the specific DTA of your home country.

3. The Myth: "I'll just issue an invoice to the agency"

A frequently heard piece of advice for supposedly avoiding the tax burden is that the foreign owner writes a direct invoice to a Spanish rental company (Explotadora), instead of the agency renting out on the owner's behalf. Attention: This model entails massive risks.

Value Added Tax (IVA) liability: If you hand over your property completely to a company for tourist sub-letting, the IVA exemption for purely residential purposes no longer applies. You must add 21% Spanish Value Added Tax (IVA) to your invoices (confirmed by binding rulings of the DGT, e.g., Consulta Vinculante V2567-24).Commercial activity: You are suddenly no longer considered a private landlord, but an entrepreneur. This means you must register for tax purposes as an entrepreneur in Spain (Alta en IAE), submit regular IVA declarations, and are subject to much stricter bookkeeping obligations.

Conclusion: This structure does not prevent double taxation regarding income tax, but merely creates a complex, IVA-liable corporate structure that is extremely unprofitable and bureaucratically cumbersome for most private holiday home owners.

4. Regional Specifics: Rental License in ValenciaThe Generalitat Valenciana has massively tightened the rules for holiday accommodations. Without an official registration number, legal renting is not possible.

Compatibility report: Without a prior, positive report from the respective municipality regarding urban planning suitability, no license will be granted anymore.Liability: Anyone who rents out without a license risks heavy fines in the Valencia region. In addition, portals require the mandatory deposit of the valid license number.

5. New, Simplified Deadlines for Modelo 210There is good news for non-residents since 2024: The tax authority has simplified the reporting obligations.

Rental income (Agrupación anual): While these previously had to be reported quarterly, rental income can now be conveniently summarized annually (for accruals from 2024 onwards). The deadline for submission is January 1st to 20th of the following year.Personal use: For the days of the year when the property was not rented out, a personal use tax applies. This can be declared throughout the entire following year (until December 31st).

Strategic Consulting by Matzon Properties

Buying a property in the Valencian Community is an excellent decision for building your wealth – if the framework conditions are right.

At Matzon Properties, our service does not end with the signature at the notary.We see ourselves as your long-term partner. Since tax complexity (especially for non-residents from Switzerland or the UK) and the issues of double taxation have a massive impact on your net yield, we work together with an exclusive network of highly specialized tax experts and lawyers (Asesores Fiscales).

Your advantage with Matzon Properties:

º Holistic approach: We examine the potential and legal feasibility of a rental license even before the purchase.

º Expert network: We connect you directly with professionals who will handle your Spanish tax return in a legally secure manner, optimize double taxation for you, and protect you from expensive models (such as incorrect invoicing).

º Security: Avoid expensive mistakes when registering and taxing your holiday property.

Do you want to ensure that your investment on the Costa Blanca or in Valencia is optimally structured from a tax perspective and legally secure from the very beginning?

👉 Click here: Contact Matzon Properties – We activate our expert network for your success! 👈

Legal Notice & Disclaimer

This article was created to the best of our knowledge and serves general information purposes. It does not replace individual tax or legal advice. Tax laws and regional regulations in the Valencian Community are subject to change. We assume no liability for the timeliness or accuracy. It is strongly recommended to consult a qualified expert for tax returns and license applications.

Sources & Official References Used:

Agencia Tributaria Española (AEAT):Official guidelines on IRNR for non-residents & deadline changes (Modelo 210 / Agrupación anual)

Dirección General de Tributos (DGT):Portal for binding rulings - Ref. V2567-24 on the tax treatment and 21% IVA for rental companies

Ministerio de Hacienda: Current Double Taxation Agreements (DTA) between Spain and Germany / Switzerland / UK

Boletín Oficial del Estado (BOE):Ley 15/2018 de Turismo, Ocio y Hospitalidad de la Comunidad Valenciana (Regulations for Vivienda Turística)

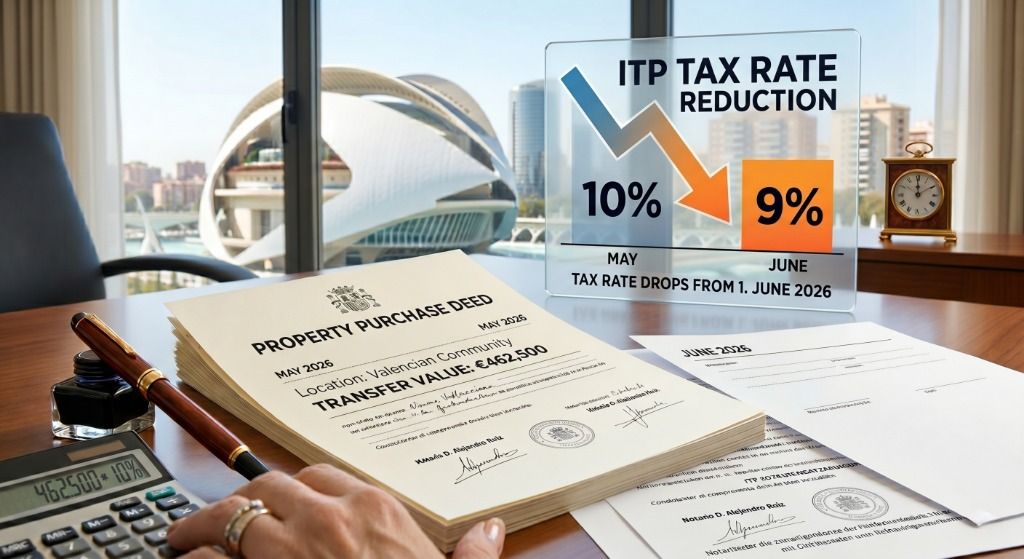

Property Transfer Tax in Valencia 2026: Save on Your Property Purchase from June

Anyone planning to buy a property on the Costa Blanca or in the city of Valencia should keep a close eye on the calendar. As of June 1, 2026, significant changes to the Property Transfer Tax (ITP...

more

Easter on the Northern Costa Blanca: A feast for the senses (2026)

Celebrating Easter on the Costa BlancaWhen the scent of incense drifts through medieval streets and the rhythmic beat of drums fills the evening air, one of the most impressive times of the year...

more

Spanish for buying property in Spain – The most important phrases for buyers on the Costa Blanca

Anyone looking to buy a property on the Costa Blanca primarily focuses on location, price, property condition, and additional costs when buying a home in Spain. However, one question is often...

more_2.jpg)

Living in Benissa Costa - Quiet Residential Areas & Sea Views

Marina Alta Town Series – Coastal Towns | Part 5: Benissa CostaBenissa Costa is considered one of the quieter and more exclusive residential areas on the northern Costa Blanca. Unlike traditional...

more